There’s been a lot of talk about mortgage interest rates lately, so it’s a good time to talk about how is mortgage interest calculated.

Mortgage interest is one of the most significant expenses of borrowing money to buy a home, but without it, you couldn’t own a home, so it’s a necessary evil. However, you should understand mortgage interest and how it works before borrowing a mortgage.

So here is the mortgage interest rate explained, so you can enter your next mortgage financing transaction as an informed borrower.

What is Interest on a Mortgage?

You might wonder what interest is on a mortgage.

Think of it like a fee for borrowing money. Just like banks pay you an interest rate to borrow the money you put in your bank account, the same is true when they lend you money.

Because a mortgage loan is usually for a long term, such as 30 years, lenders must charge interest to cover their cost of lending you the money or the opportunity cost of not having the funds for the next 30 years.

Mortgage interest is expressed as a percentage of your loan amount. The higher the interest rate a lender charges, the more interest charges you pay.

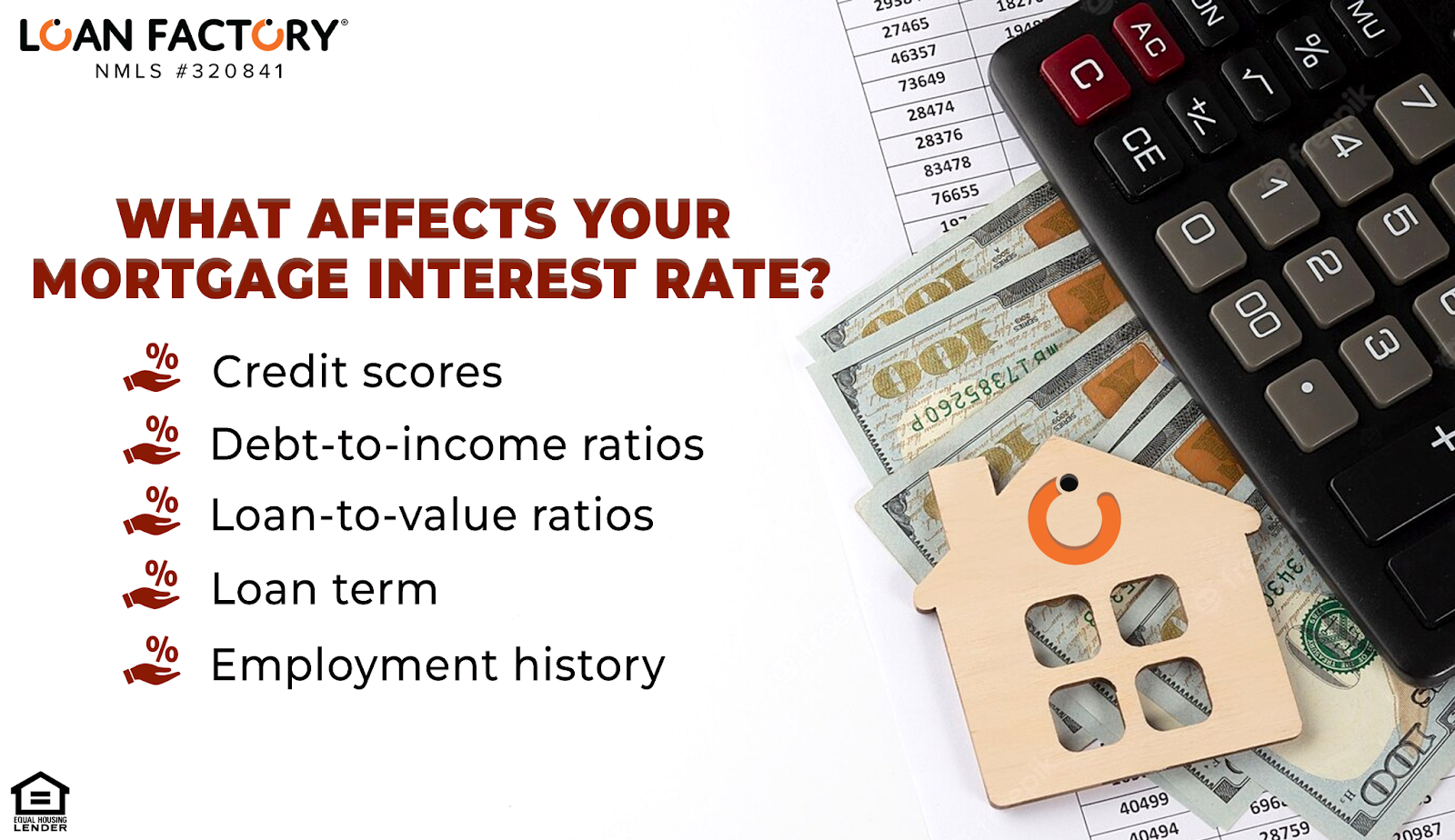

What Affects Your Mortgage Interest Rate?

So you know everyone must pay interest, but what affects how much you pay? Unfortunately, no two lenders typically have the same rates or terms, so here’s what might affect the rate a lender offers you.

- Credit scores

If you have a high credit score, you are at a lower risk of default for lenders. Good credit signifies you pay your bills on time and don’t default. Lenders like this and might reward you with a lower interest rate than someone who doesn’t have a good credit score.

- Debt-to-income ratios

Your DTI compares your monthly obligations to your income before taxes. A high DTI means you have a lot of your income already committed to debt obligations, and a low DTI means you have more disposable income.

Each loan program has a maximum DTI, but if you have a debt ratio much lower than the maximum allowed, you may get a lower interest rate.

- Loan-to-value ratios

Your LTV measures the loan amount to your home’s value. The higher the LTV, the higher the risk you pose because you have less of your money invested in the house. Conversely, a lower LTV will typically get you a lower mortgage rate.

- Loan term

The longer you borrow money, the higher your risk to the lender. For example, 15-year loans usually have much lower interest rates than 30-year loans and vice versa. The less time you have the lender’s money, the less you’ll pay in interest.

- Employment history

Lenders like borrowers with a stable employment history. They look back over the last two years, looking for you to be at the same job. If you have an even longer history than two years and increasing income, it lowers your risk of default which might mean a lower interest rate.

How is Mortgage Interest Calculated by your Lender?

There are multiple factors lenders consider when calculating your mortgage interest and payment.

First, lenders assign an interest rate to your mortgage. Let’s say, for example, they chose a 5% rate for your loan. Next, they amortize your principal (the amount you borrow) over the loan term, say 30 years.

The lender calculates the monthly interest payment based on the outstanding principal balance. So, in the first month, most of your payment goes to interest, with a slight amount covering the principal.

The following month, you’ll pay a few pennies less in interest because you lowered the principal balance slightly. This continues until you pay off the loan in full; each month you’ll pay a slightly lower amount of interest and higher principal.

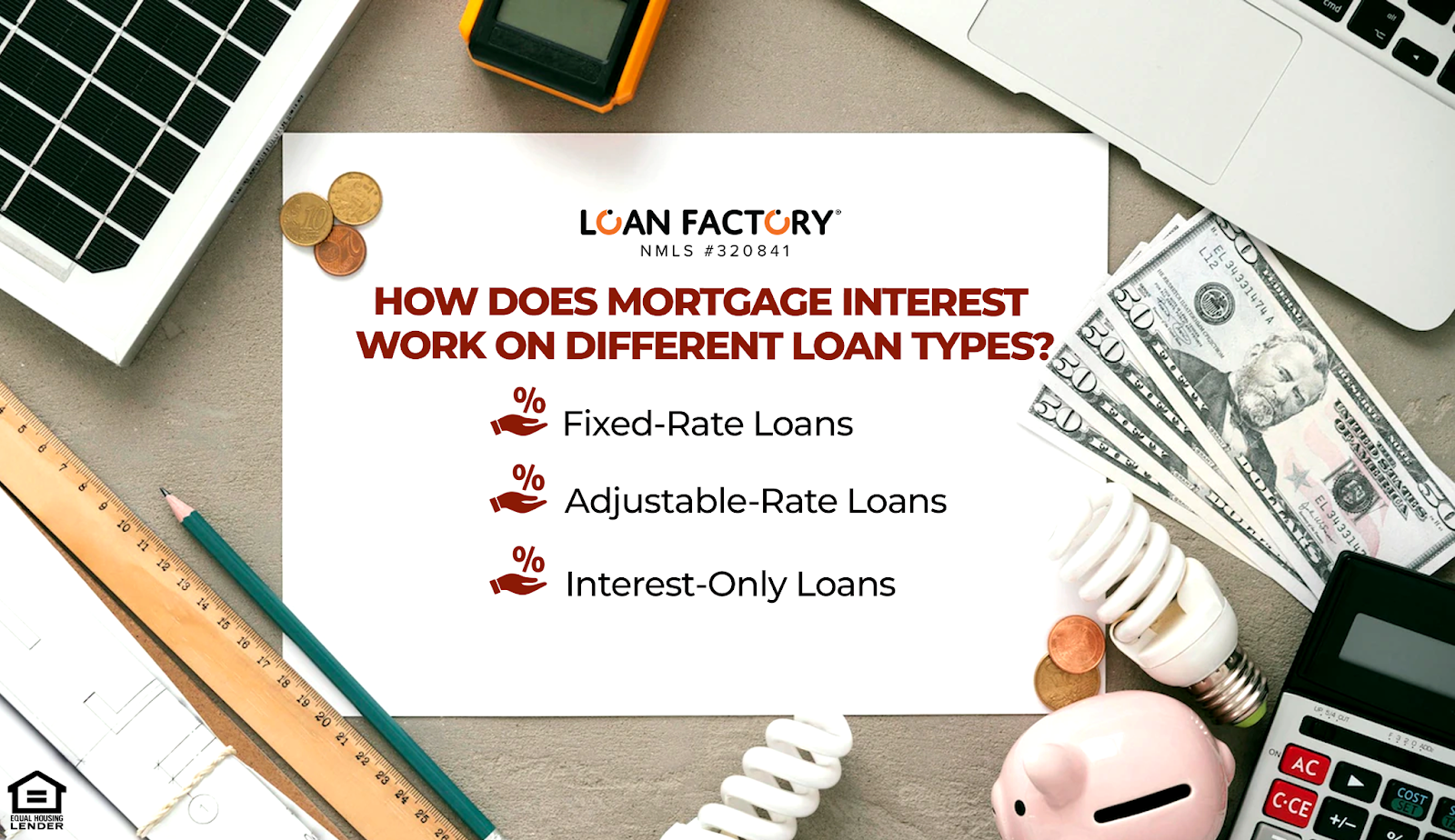

How Does Mortgage Interest Work on Different Loan Types?

Home interest calculations work differently depending on the type of mortgage loan you have. Borrowers can choose a fixed-rate, adjustable-rate, and sometimes an interest-only loan.

Fixed-Rate Loans

Fixed-rate loans have the same mortgage payment for the life of the loan. The only thing that changes is the amount of your payment that goes toward interest or principal.

As we said earlier, at the start of a mortgage, most of the payment covers interest. As you pay the principal balance down, the interest payments decrease, and the principal payments increase.

Adjustable-Rate Loans

Adjustable-rate loans have a fixed rate for a short period and then adjust annually. This means your mortgage payment can change yearly depending on how rates perform.

Like a fixed-rate loan, a portion of your payment covers the interest payment, and the rest covers the principal. Some years you might pay more principal than others; it depends on how much interest rates increase or decrease each year.

Interest-Only Loans

Interest-only loans are a non-QM loan option and allow you to make interest-only payments for a few years. However, it’s a fixed period in which you are only obligated to pay interest, and afterward, you must begin paying principal and interest to pay the loan in full by the end of the term.

Final Thoughts

As you wonder how is mortgage interest calculated, know that a lower interest rate is better than a higher one when you can help it. However, everyone pays interest when they borrow money, whether it’s a mortgage, personal loan, or a loan to buy a car.

The key is to perfect your qualifying factors to get the most attractive interest rate possible. This way, you minimize your interest cost and increase your loan’s affordability.

Contact Loan Factory today if you have any questions about the mortgage interest calculation or how to get the most competitive interest rates.