Homebuyers that don’t fit the ‘typical mold’ of mortgage requirements often find that they can’t get a mortgage. With tighter mortgage guidelines, many potential borrowers find themselves without the necessary financing, especially since the housing crisis of 2008. With tighter restrictions, more borrowers are pushed out of a possible loan.

This makes borrowers wonder if they don’t meet the requirements, can they not buy a home?

Fortunately, there’s a solution called a non-QM or non-qualified loan. It sounds ‘bad’ or like something that helped cause the housing crisis, but they aren’t. Today’s alternative loans aren’t risky, and when you work with the right lender, they can be a great solution to your mortgage financing needs.

Here’s what you must know.

What are Non-QM Loans?

The Consumer Financial Protection Bureau creates guidelines for loans to be called qualified loans. This means the loans meet the ability to repay rule and the lender verified the borrower’s income beyond a reasonable doubt. In addition, lenders must prove they did their due diligence to ensure you can afford the loan.

Some of the most important guidelines surround your income, such as what you provide to verify it and how you earn it. For example, if you can’t provide paystubs and W-2s or tax returns, you won’t fall under the Qualified Mortgage guidelines, but you might qualify for a non-QM loan.

A non-qualified loan means the loan either has riskier features than is allowed with qualified loans or the lender accepts an alternative form of income verification.

How do Non-QM Loans Work?

Non-QM loans don’t fall under specific guidelines, so the requirements or features may vary, but here are some options for the non-QM loan type.

- Loan term longer than 30 years – If you need a smaller payment, you may need to amortize your loan over a longer period. Qualified mortgages only allow terms up to 30 years, but non-QM loans can offer terms as long as 40 years.

- Interest-only payments – When you have an interest-only mortgage, you must only cover the interest portion of your payment for a certain length of the term. This means your loan balance doesn’t decrease until you start making principal payments. For some, this is risky, but if you have a job with income that will significantly increase in a few years, it could work well.

- Balloon payments – It’s rare, but some people prefer a balloon loan with a lump sum due at the end of a short term, while the loan is amortized over a 30-year term.

- Alternative forms of income verification – This is the bread and butter of non-QM loans. Borrowers who can’t verify their income the traditional way can use a non-qualified loan to verify their income with bank statements or other alternative methods.

- Looser credit requirements – Qualified mortgages require certain waiting periods after a significant credit event, such as bankruptcy or foreclosure. However, non-QM loans can offer a mortgage as soon as one day after if the lender allows it.

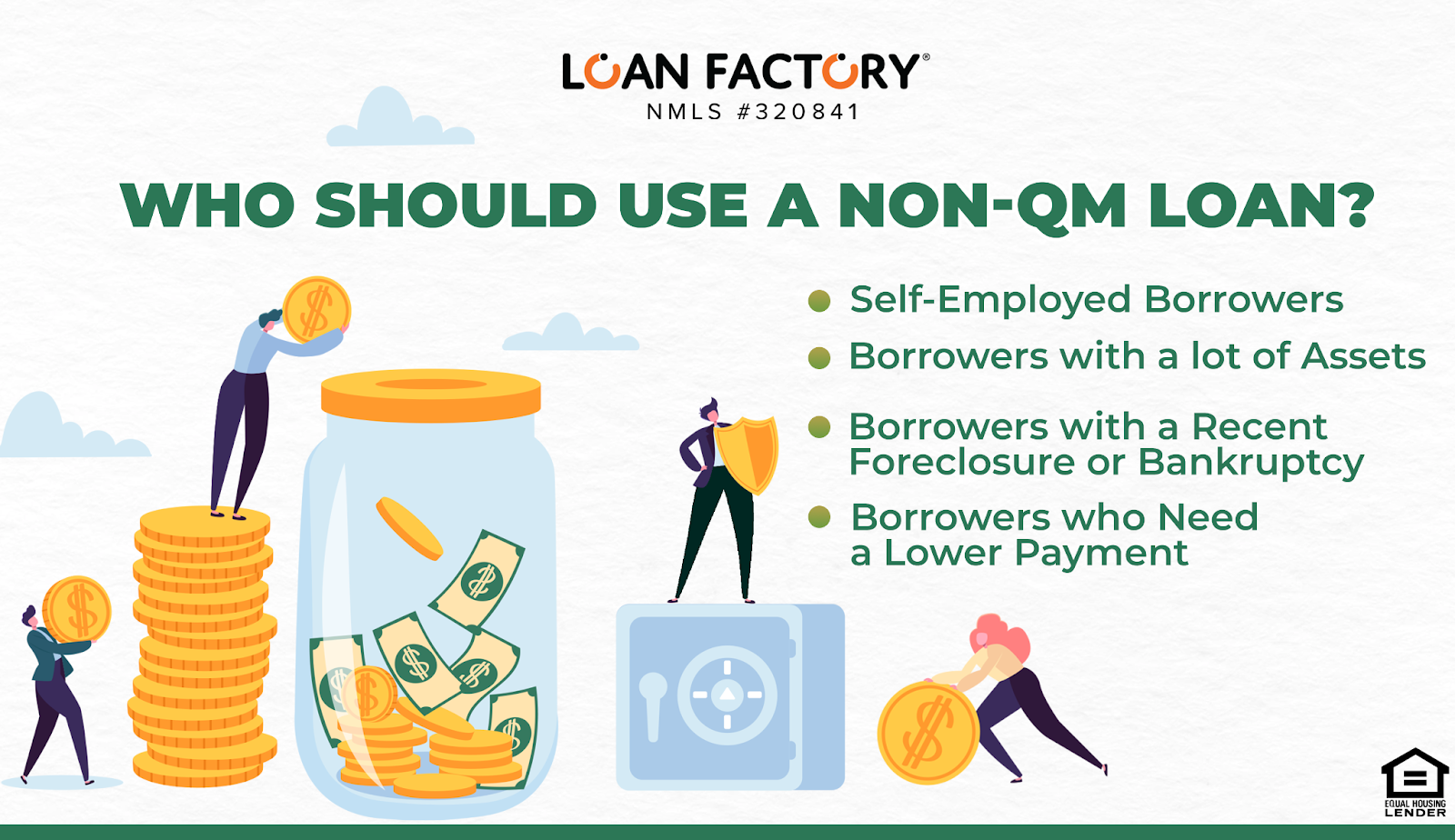

Who Should Use a Non-QM Loan?

Clearly, non-QM loans are riskier than qualified mortgages, so who should take advantage of them?

Several types of borrowers benefit, including the following.

Self-Employed Borrowers

Self-employed borrowers use non-QM loan types quite often. Here’s why.

Lenders must use the adjusted gross income reported on a borrower’s tax returns. If you own a business, you likely take as many deductions as possible to reduce your tax liability. While that’s great for your taxes, it looks like you don’t make enough money on paper for a QM loan.

Non-QM loans allow the use of bank statements and other alternative documentation to prove you make enough money to afford the loan.

Borrowers with a lot of Assets

If you don’t work and instead live off your assets, you may have plenty of money to afford a loan, but on paper, you don’t.

Qualified mortgage lenders can’t accept bank or investment statements to prove your income, but non-QM lenders can. Typically, they use the asset depletion method, which divides their assets up equally among the term. So, for example, for a 30-year term, they would divide the total assets by 30, using that number for the annual income.

Borrowers with a Recent Foreclosure or Bankruptcy

If you had a recent adverse credit event, you wouldn’t qualify for a QM loan for a few years. However, if your housing needs are more pressing, you might qualify for a non-QM loan since there aren’t requirements regarding how long you must wait to get a loan.

Borrowers who Need a Lower Payment

If you are in a high-income job but starting with a lower salary, you may need a lower mortgage payment now but can afford a higher payment once your income increases.

This is common for doctors and lawyers just out of school. They need a place to live and want to own a home but don’t have the high income they were promised. An interest-only loan can help them qualify for the mortgage now and know that they can afford the full payment in the future.

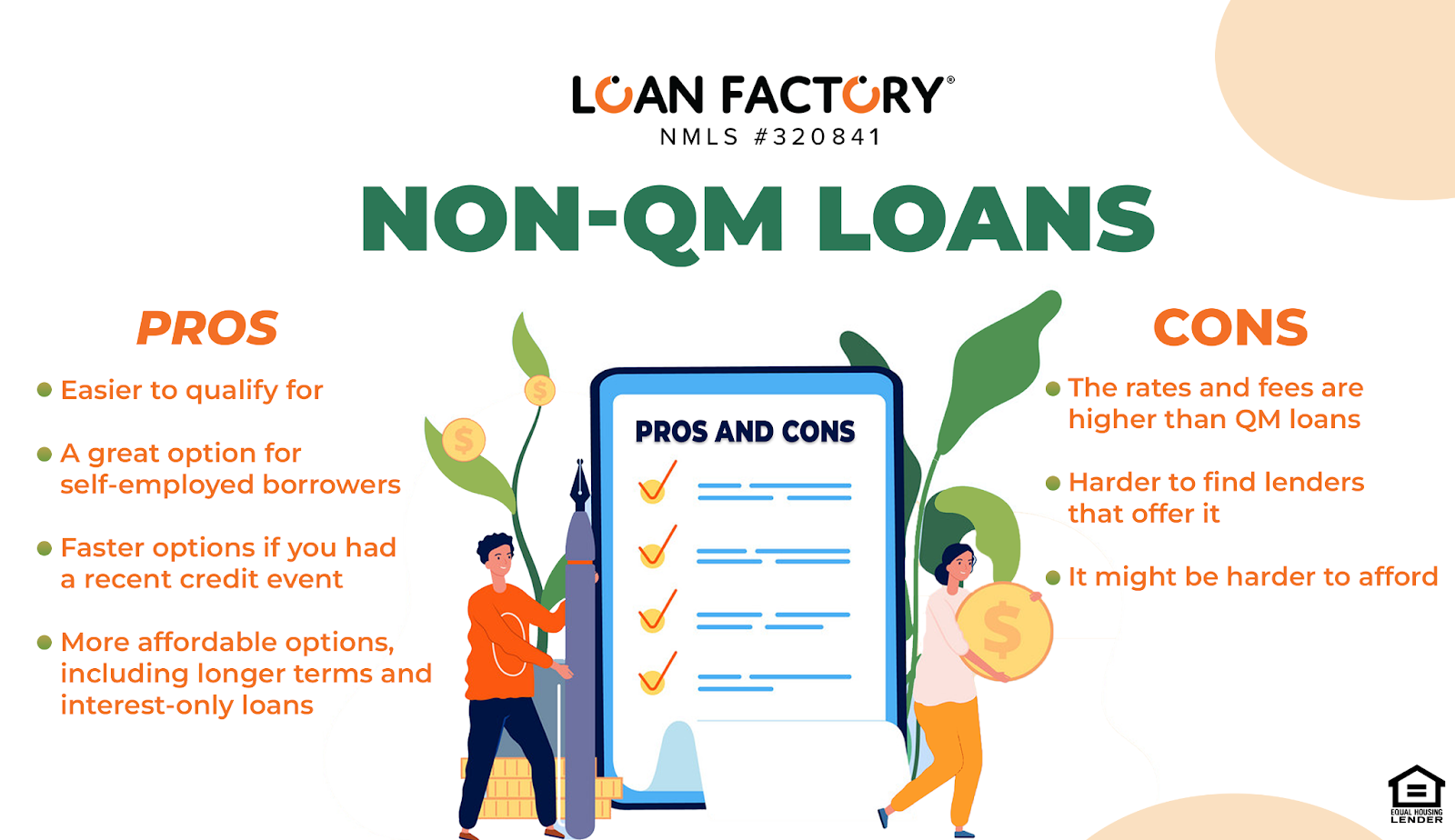

Pros and Cons

All loan programs have pros and cons. Here’s what you should know about non-QM loans.

Pros:

- Easier to qualify for

- A great option for self-employed borrowers

- Faster options if you had a recent credit event

- More affordable options, including longer terms and interest-only loans

Cons:

- The rates and fees are higher than QM loans

- Harder to find lenders that offer it

- It might be harder to afford

Final Thoughts

Before you apply for a non-QM loan, exhaust all of your options. If you know you won’t qualify because you’re self-employed or had a recent credit event, work with a reputable lender like Loan Factory to ensure you’re getting a loan you can afford and that has the most competitive terms.